Servizi

Buckley Capital Management Sends Letter to Basic-Fit's Board and Management Recommending Strategic Review with the Intention to Sell the Business

Dear Members of the Board of Directors and Management:

Buckley Capital Management, LLC, together with its affiliates (collectively, "we" or "Buckley"), is a long-term shareholder of Basic-Fit NV ("Basic-Fit" or the "Company").

As you know, Buckley Capital Management is a Miami -based investment firm specializing primarily in North American small and mid-cap value stocks. Our focus is on identifying and investing in high-quality companies with strong growth potential trading at an attractive value multiple. This typically means businesses that are trading below 10x earnings that are growing earnings more than 10% per year. The average PE multiple in our portfolio today is 9x with a 17% average earnings growth rate. We collaborate closely with boards and management teams to unlock value and drive sustainable long-term growth, benefiting all shareholders. We are trusted to manage capital on behalf of family offices, foundations, ultra-high net worth and high net worth individuals. In addition, with 95%+ of our Partners' investable net worth committed to our funds, we ensure a strong alignment of interests with our investors and the companies in which we invest.

We have valued our ongoing dialogue with Basic-Fit's Chief Financial Officer, Hans Van Der Aar, and Investor Relations Manager, John David Roeg since August 2022 , during which we have raised concerns and offered recommendations to drive the Company's long-term growth. In our most recent meeting on August 26 , 2024 in Amsterdam , we were disappointed to hear of the management's lack of interest in exploring a sale of the Company, especially given the significant value this would unlock. Based on conversations we have had with various industry participants, we are confident that there is significant interest from private equity , and we would implore Basic-Fit's management and the Board to initiate a strategic review process.

Despite Basic-Fit's position as an industry leader[1] and its track record of growth, the Company continues to be significantly undervalued by the public markets. It is incumbent upon Basic-Fit's Board of Directors to determine the optimal path forward to create value for stakeholders, and we expect the Board to be open-minded about different strategic opportunities for change. In our view, Basic-Fit has a set of highly valuable assets that position the Company well to operate as a private entity, and it is important for the Board to consider the potential value-creation opportunities that a sale of the Company could offer.

We have decided to release this letter publicly to initiate an open dialogue about our recommendation. By involving all stakeholders in this conversation, we can ensure that everyone has the opportunity to consider our views and offer input on how best to drive long-term value.

We initially decided to invest in Basic-Fit in August 2022 due to the high prospective growth rate in the business, the consistency and predictability of the business model, and the long runway for growth. Today, we are a top 20 shareholder, owning approximately 0.78% of the issued and outstanding shares in the capital of Basic-Fit.

Basic-Fit is an expanding business in the growing European low-cost fitness market. Since its IPO in June 2016 , Basic-Fit has been growing the business at around 20% annualized, with an outstanding track record of growth across all of its major KPIs[3]. During this period, and including the COVID pandemic years, Basic-Fit has grown its club base at a 19% CAGR, memberships at a 19% CAGR, revenues at a 22% CAGR, and underlying EBITDA less rent at 18%.[4]

Basic-Fit has combined two important business concepts—the low-cost consumer-facing business, which includes some of the most significant value creators within the consumer space, such as Walmart, Amazon, and Costco; and the concept of local network effects and economies of scale, as seen in the telecom and cable industries—to create the leading low-cost gym operator in continental Europe . With approximately 1,500 gyms across six countries, it is the industry leader by a significant margin, with a Company footprint about three times the size of its next largest European competitor and about equal to the top three combined[5]. It operates the largest low-cost fitness network in each of France , Spain , Belgium , Luxembourg , and the Netherlands , and has a rapidly growing Germany segment. With strong competitive advantages and significant brand awareness, the Company's mature clubs sustain strong unit economics, operating at over 45% EBITDA margins and 30% returns on invested capital.[6]

The Company's strong growth is expected to continue in the near future, with analyst consensus[7] estimates for underlying EBITDA less rent expected to grow ~22% to a new record of €317 million in 2024 and to increase an additional 22% in 2025 to €386 million.

Over the next decade, Basic-Fit's future will be even more exciting. Despite the Company's great success in growing its industry, fitness membership penetration remains relatively low in most of its European markets. Compared with 22% in the United States , fitness penetration in the Netherlands is 18%, in Denmark 13%, in Spain 12%, in France 11%, and in Belgium just 9%.[8] Increases in penetration will in our view also be fueled by increased awareness of health and wellness among millennials and Generation Z. With its very high returns on capital in its existing markets, Basic-Fit has a long runway to deploy capital in line with these trends. Moreover, the Company is exploring the possibility of franchising its brand in new markets, which will add to growth and margins.

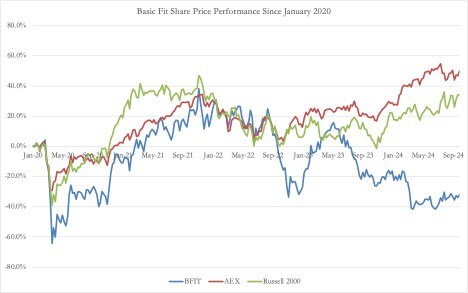

Despite this rapid and high-quality historical growth and its great potential for future growth, Basic-Fit's stock has significantly underperformed indices and peers in the consumer discretionary vertical. As shown below, since January 2020 , Basic-Fit's market price has declined 34%, underperforming the broader comparable market.

Infographic -

https://mma.prnewswire.com/media/2518745/Bloomberg_Data_Infographic.jpg

Source: Bloomberg Data

{kind=link}

Due to this underperformance, Basic-Fit now trades at just 6.5 times its next-twelve-month EBITDA estimates, a nearly 60% discount to comparable consumer discretionary companies serving a lower income consumer operating in North America and Europe.[9] Notably, the current share price does not even properly value the underlying profitability of Basic-Fit's club network at its current size, before considering growth from future new club additions.[10]

Source: Capital IQ

We believe this undervaluation exists largely because of perception issues caused by recent shortfalls relative to short-term market expectations, as well as public investors' misunderstanding of the company's financial structure, particularly the distinction between financial debt and lease obligations. We believe investors are far too focused on immaterial short falls in the business, such as a small miss in FCF/share guidance in 2024, which has led to the share price being down almost 50% compared to its peak levels in 2022. While Basic-Fit has not hit every public guide it has put out, it has come close and grown the business at an extremely attractive long-term rate. [11]

We do not view Basic-Fit as a company burdened by financial constraints that must seek a private equity lifeline. Rather, we view going private as a proactive opportunity for Basic-Fit to achieve several compelling goals:

1. Better execute its growth strategy without pressures from short-term market expectations

2. Achieve greater operational flexibility; to gain sharper focus on long-term value creation

3. Provide more strategic options for financing growth.

As evident in its past track record, Basic-Fit has the potential to thrive as a private entity. As a private company, Basic-Fit would be able to grow at a faster pace to capture additional market share and focus more on the long-term strategic goals that are in the best interest of the Company, without being constrained by the short-term pressures of the public markets. This would be beneficial for the Company and the owners of the business given the 30% ROIC[12] on new gyms, but also Basic-Fit's employee base given the growth would create more jobs, increase stability, and free up more resources to dedicate to employee benefits, training and development programs.

We believe the gap between Basic-Fit's current valuation and its significant long-term upside will allow a private buyer to make an offer for the Company at a significant premium to today's stock price while still generating a substantial expected rate of return on its purchase price. As a starting point, simply multiplying the Company's current club base (1,500) by its guidance for the underlying EBITDA less rent of a mid-term mature club (€460,000) yields an aggregate underlying potential profit of close to €700 million, which is more than twice its current reported underlying EBITDA less rent.[13] If Basic-Fit hits its goal of 3,000 mature gyms by 2030, then assuming the same per-gym profitability it could generate €1.4 billion of EBITDA.[14] At 12 times EBITDA, Basic-Fit would then be worth ~€17 billion, representing 600%+ upside from today's levels excluding the value of cash generated more than capex needs.[15]

As an alternative valuation framework, we see Planet Fitness as the best comparison for Basic-Fit, as the two companies have two very similar business models operating on two separate continents. Individual Planet Fitness locations tend to sell for around 7 times EBITDA. However, if individual locations are aggregated into a group of locations, the resulting diversification of individual-location risks will increase the group's transaction multiple in both public and private markets as it gets larger. As a result, Planet Fitness groups tend to sell for anywhere between 8-10 times EBITDA depending on their forward growth expectations.

A Planet Fitness group with similar growth to Basic-Fit would trade near the high end of this range, around 10 times EBITDA. Given that Basic-Fit is significantly larger than any one group of Planet Fitness locations with faster growth projected, we believe 10 times EBITDA would be the absolute lowest multiple that Basic-Fit would fetch in a private sale. Historically, Basic-Fit has traded near the levels we would expect in the private market, at 10-13 times EBITDA. In this context, the Company's recent trading range of 6-7x forward EBITDA is shockingly low given its size, high free cash flow conversion, and very long runway for future growth. But it also gives any private equity buyer ample room to offer a significant premium to all Basic-Fit shareholders to take the Company private.

Employees would also benefit significantly from private equity interest, as the business would be able to focus on its long-term strategy and growth, unconstrained from the desires of public markets investors. This would ultimately create greater operational flexibility, more jobs and advancement opportunities, as well as additional resources to invest in employee benefits and development.

Following our past conversations, we believe that now is the time for Basic-Fit's Board of Directors and management to take action to maximize long-term value for all of its stakeholders, including shareholders. As outlined in this letter, Basic-Fit is fundamentally misunderstood by public markets and has the potential to thrive again under private ownership. As such, we strongly encourage the Board to launch an immediate strategic review to seriously consider a sales process for the Company.

We look forward to maintaining a collaborative and productive relationship with the Board and management to drive shareholder value and are eager to continue our meaningful discussions.

Sincerely,

Managing partner

Zack Buckley

Buckley Capital Partners LP

Buckley Capital is a Miami -based investment firm specializing primarily in North American small and mid-cap value stocks, regulated by the SEC.

Contacts

For Investors:

Buckley Capital Partners LP

Zack Buckley

For Media:

Greenbrook

Rob White / Teresa Berezowski

BuckleyCapital@greenbrookadvisory.com

[1] Basic-Fit Public Filings

[2] Basic-Fit Public Filings

[3] Basic-Fit Public Filings

[4] Basic-Fit Public Filings

[5] Basic Fit Public Filings

[6] Basic-Fit Public Filings

[7] Corporate.basic-fit.com

[8] Basic-Fit Public Filings

[9] Bloomberg, Capital IQ, and Basic-Fit Public Filings

[10] Basic-Fit Public Filings

[11] Basic-Fit Public Filings

[12] Basic-Fit Public Filings

[13] Basic-Fit Public Filings

[14] Basic-Fit Public Filings

[15] Basic-Fit Public Filings

View original content to download multimedia: https://www.prnewswire.com/nl/persberichten/buckley-capital-management-sends-letter-to-basic-fits-board-and-management-recommending-strategic-review-with-the-intention-to-sell-the-business-302261902.html